What if the only thing standing between you and a $150,000 high income career is a single math equation you haven’t mastered yet? You aren’t alone if you feel buried by complex spreadsheets and shifting benchmarks. It’s exhausting to chase a target when the dealership keeps moving the goalposts. You deserve to know exactly how every deal impacts your bank account. Stop guessing. This guide provides the f&i manager commission structure explained with total clarity so you can take control of your financial future.

We’ll show you how to push your Profit Per Variable Retail (PVR) past the $1,500 mark and boost your product penetration to 2.0 or higher. You’ll unlock the blueprint to maximize your earnings and gain the confidence to negotiate a pay plan that rewards your talent. We are diving into the specific tiers, percentages, and performance metrics that the top 10% of earners use to build lasting wealth in the F&I office. Get ready to master your potential.

The F&I Manager is the undisputed profit engine of the modern automotive dealership. While sales teams focus on moving metal, the finance office focuses on generating the “backend gross” that keeps the dealership profitable. It’s a high-stakes environment where your ability to close determines your lifestyle. You aren’t trading time for money here. You are trading results for a high-income career. By 2026, industry data suggests that trained F&I professionals in high-volume stores will see average compensation packages exceeding $185,000, with top performers frequently breaking the $250,000 barrier. This isn’t a job for the complacent. It’s for the ambitious.

Understanding the f&i manager commission structure explained starts with a radical shift in your mindset. You must move away from the flat salary security blanket found in retail or entry-level roles. In the F&I office, your paycheck is a direct reflection of your efficiency and your ability to sell intangible value. You manage the delicate balance between lender requirements and customer needs. To truly excel, you need a solid foundation in how Car Finance Explained works, including the mechanics of interest rate markups and service contract margins. This knowledge allows you to maximize the backend gross on every deal that crosses your desk.

The backend gross is the foundation of your wealth. It consists of the profit made on financing, insurance products, and extended warranties after the vehicle price is already settled. In many dealerships, this profit center accounts for over 55% of the total operating income. You are the gatekeeper of this revenue. If you don’t perform, the dealership doesn’t thrive. That’s why the F&I manager is the most sought-after and protected position in the building.

Many professionals start on the sales floor, but the real money lives in the finance office. It’s common for a top-performing F&I Manager to out-earn the General Sales Manager (GSM). While the GSM manages people and inventory, you manage legal compliance and bank relations. You hold the power to get a deal bought or buried. This level of responsibility commands a premium price. You are an expert in consumer law and credit tiering. If you want to know more about the daily grind, check out our guide on What is an F&I Manager? to see if you have the drive to succeed.

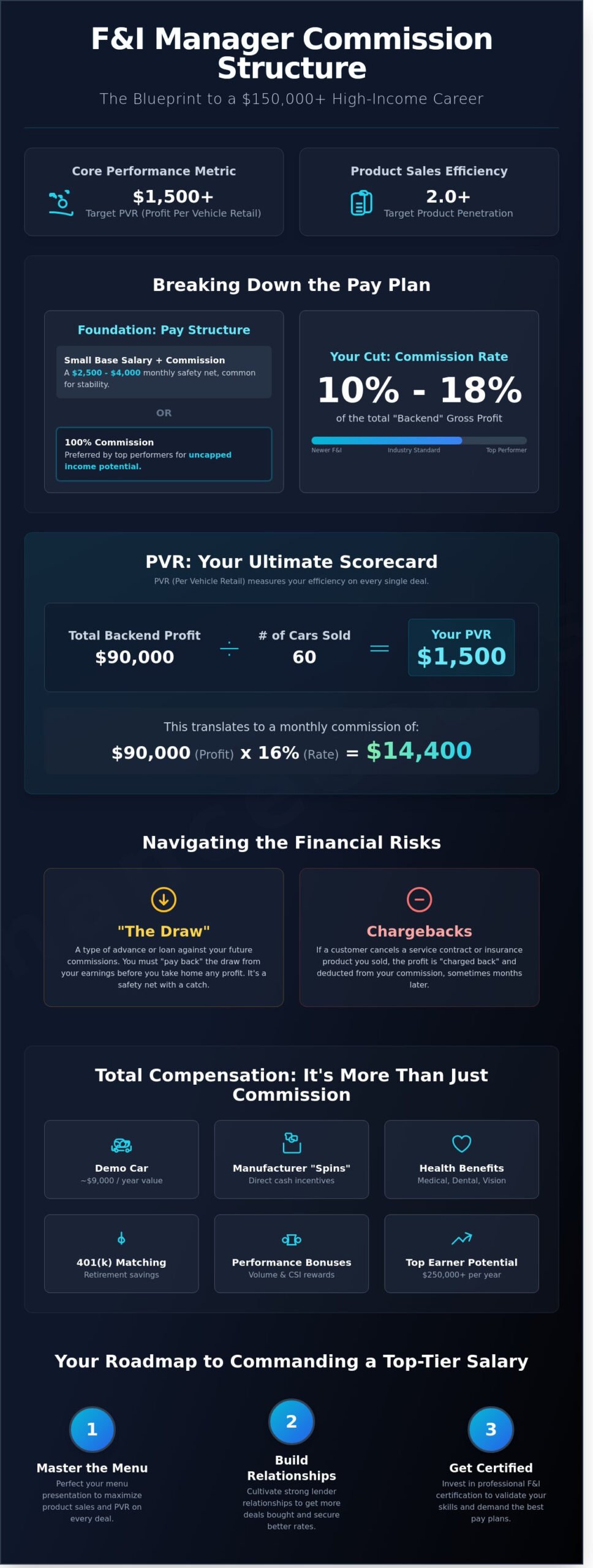

A high-income career in F&I offers more than just a commission check. Most dealerships provide a demo car, saving you roughly $9,000 annually in vehicle payments, maintenance, and insurance. You also gain access to manufacturer spins. These are direct cash incentives from car makers or warranty companies for hitting specific volume targets. When you add health benefits, 401k matching, and performance bonuses, the total package is staggering. This role isn’t just a step up; it’s a total transformation of your financial future. Are you ready to master these skills and claim your seat in the office?

Your paycheck isn’t a mystery; it’s a math equation. To master the f&i manager commission structure explained here, you must first understand the foundation of dealership compensation. Most elite F&I offices operate on a “draw against commission” or a small base salary, typically ranging from $2,500 to $4,000 per month. This acts as a safety net during slow seasonal months like January or February. However, the real money lives in the backend gross. High performers often prefer 100% commission structures because they provide an uncapped ceiling for their income potential. If you’re confident in your skills, you’ll want the highest percentage possible rather than a guaranteed base.

The standard industry commission rate fluctuates between 10% and 18% of the total backend profit. If you generate $100,000 in monthly profit for the dealership, a 15% pay plan puts $15,000 in your pocket. This profit comes from two primary sources: the finance reserve and product sales. Understanding the F&I Department’s Role is crucial. It involves balancing lender relationships with customer needs to maximize these margins while staying compliant. Dealers track these numbers daily to ensure the department remains the most profitable square footage in the building.

PVR is the total backend profit divided by the number of units sold. It’s the ultimate scorecard for your efficiency. Let’s look at the numbers. If you average a $1,500 PVR and settle 60 deals in a month, you’ve produced $90,000 in gross profit. At a 16% commission rate, your monthly take-home is $14,400. You’ll need to distinguish between Finance Reserve and Product Profit. Finance Reserve is the “spread” or “markup” on interest rates. Product Profit comes from service contracts and GAP. Top-tier managers aim for a 70/30 split. This means 70% of the profit comes from products, which ensures more stable income and higher customer satisfaction scores.

Dealers reward balance through “Step-Up” structures. You don’t just get paid on the gross; you get paid more for selling specific items. For instance, hitting a 50% Vehicle Service Contract (VSC) penetration rate might “step up” your entire commission from 14% to 16% retroactively for the whole month. This incentivizes you to protect every customer. Ancillary products like tire and wheel, key replacement, and paint protection aren’t just add-ons. They’re the building blocks of a high-income career. Using a structured “Menu” approach ensures every client sees every product. This is the fastest way to increase your PVR and maximize your earnings without spending more hours at the desk.

Success in this role requires more than just luck. It requires a deep understanding of how these tiers interact. When you combine high PVR with 2.0 product penetration, you become an indispensable asset. Are you ready to master these metrics? The difference between a $60,000 salary and a $180,000 income is simply the ability to execute this f&i manager commission structure explained in every single deal. You have the potential to drive your career forward by mastering these numbers today.

Understanding the f&i manager commission structure explained starts with mastering “the draw.” Most dealerships pay you an advance against your future earnings. This isn’t a base salary. It’s a financial safety net. If your draw is $4,000 monthly and you generate $15,000 in gross profit commission, you receive the $4,000 advance plus an $11,000 commission check. If you hit a slow cycle and only earn $2,500, the dealer still pays you the $4,000. However, you’ll start the next month $1,500 “in the hole.” Top performers rarely worry about the draw because their consistent volume keeps them well above the floor.

Chargebacks represent the biggest threat to your paycheck. When a customer cancels a Vehicle Service Contract (VSC) or GAP insurance 60 days after the sale, the lender claws back the commission from the dealership. The dealership then claws it back from you. To mitigate this risk, most stores implement a chargeback reserve. They typically withhold 10% to 12% of your monthly earnings in a separate account. This reserve acts as a buffer. According to data and best practices from the National Automobile Dealers Association, maintaining high ethical standards and clear disclosures reduces these profit leaks significantly. If your reserve account exceeds a set cap, like $10,000, you usually receive the overage in your regular pay cycle.

Legal compliance is your ultimate shield. If you cut corners or misrepresent products, you’re inviting cancellations. A 2023 industry study showed that 22% of chargebacks stem from “buyer’s remorse” caused by high-pressure tactics. Master the legalities and you protect your income. Every document you sign must be accurate. One mistake on a truth-in-lending disclosure can void a deal and wipe out your hard-earned profit.

Stop selling products and start selling value. When a customer understands that a $2,800 VSC protects them from a $6,000 transmission failure, the sale becomes “sticky.” Use proper disclosure techniques to ensure every customer knows exactly what they’re buying. This transparency builds trust and eliminates the 30-day cancellation itch. If you want to master these high-level retention skills, check out our F&I Manager Training Your Ultimate Guide to secure your professional future.

Your performance isn’t just measured in dollars. It’s measured in surveys. Many pay plans include a CSI “kicker” or penalty. If your scores fall below the 93% regional average, the dealer might dock your total commission by 5% or 10%. You must balance aggressive product presentation with a world-class customer experience. Elite managers know that a happy customer doesn’t just mean a clean survey. It means repeat business and zero chargebacks. Don’t sacrifice your reputation for a quick buck. Prioritize the relationship to unlock long-term profitability and career stability. Your income potential is limitless when you combine sales talent with professional integrity.

Your PVR (Profit Per Vehicle Retailed) is the heartbeat of your paycheck. To dominate this field, you must move beyond order-taking and become a master of the menu. Top performers in 2024 consistently maintain a PVR above $1,800 by ensuring 100% product presentation. If you skip a product because you assume the customer won’t buy it, you’re throwing away your own money. A structured f&i manager commission structure explained through real-world results shows that skipping just one product presentation can cost a manager $15,000 in annual income. You must treat every customer as a blank slate with full profit potential.

Professional training is the only way to slash bank turn-down rates. Industry data from the first quarter of 2024 indicates that managers with formal certification see 22% fewer rejections from subprime lenders. You need to know how to “sell” the deal to the bank buyer before you ever try to sell the product to the customer. This involves collaborating with the sales floor to ensure every deal jacket arrives “clean.” Deals with 100% accurate credit applications and pre-verified income move through the system faster and with higher approval rates. High-income managers don’t wait for deals to break; they prevent the break before it happens.

The first 300 seconds in your office dictate your total commission for the month. You aren’t just checking IDs; you’re hunting for pain points. Does the customer drive 20,000 miles a year? That is your opening for a high-margin Service Contract. Are they worried about total loss? That is your GAP insurance play. Successful deal structuring starts before the customer sits down in your office. By the time they walk through your door, you should already know their credit tier, their trade-in equity position, and their likely objections. Use this time to build a bridge of trust that makes the “yes” inevitable.

Your relationship with bank buyers is a massive revenue lever. You must negotiate the “spread” between the buy rate and the sell rate with precision. While many states cap this reserve at 2.0% or 2.5%, maximizing that margin on every deal adds up to thousands in monthly reserve income. Speed is your ally here. Deals that fund within 48 hours keep your commission cycle moving and keep the General Manager happy. A deal sitting in “contracts in transit” for more than 72 hours is a deal that isn’t paying you yet.

Success in this role requires more than just luck. It requires a proven system. If you want to stop guessing and start earning, you need to Master the F&I Process Now to unlock your full earning potential and secure your high-income career.

High-earning F&I managers aren’t born; they’re trained. A dealership general manager won’t hand over a $200,000-a-month gross profit department to someone who simply hopes to learn as they go. They want proof of competence. They want a professional who hits the ground running on day one without costing the store thousands in compliance errors. When you look at the f&i manager commission structure explained throughout this guide, you realize your percentage of the profit depends entirely on your perceived value to the house.

General Managers offer the most aggressive pay plans to “job-ready” candidates who already understand menu selling and lender relations. If you walk into an interview and demonstrate you can maintain a $1,500 PVR (Per Vehicle Retail) while keeping CSI scores above the regional average, you’re no longer a risky hire. You’re an asset. The difference between a 12% commission tier and a 18% tier often comes down to the confidence you project during that first meeting.

The Online F&I Manager Course provides the exact roadmap needed to bridge the gap between “interested” and “hired.” It’s designed to simulate the high-pressure environment of a modern showroom. You’ll learn to handle objections, manage credit tiers, and finalize paperwork with surgical precision. This isn’t just theory; it’s training built from real-world F&I office experience.

By 2026, the regulatory environment for auto lending will be tighter than ever before. Dealerships face massive financial risks from improper disclosures or inconsistent deal structuring. Proving you’re certified shows an employer you understand the legal landscape. You’ll stand out in an interview by speaking fluently about Regulation Z and the Fair Credit Reporting Act. This technical knowledge gives you a massive advantage over the 85% of applicants who only have floor sales experience. Skipping the trial-and-error phase allows you to start earning top-tier commissions immediately. For a deeper dive into the specific requirements, see our guide on How to Become an Auto F&I Manager.

Consider the math behind this career move. A $499 investment in a professional certification course is a small price for a 300x return. Average F&I salaries in top-tier metro markets now exceed $150,000 annually. High-volume stores processing 100+ units a month don’t have time to teach you the basics. They need experts who can maximize every deal that walks through the door. Once the f&i manager commission structure explained above is working in your favor, that initial training cost is covered by your very first paycheck. Your career path is clear: get trained, get certified, and secure a high-income career that changes your financial future.

Are you ready to drive your career forward? Don’t wait for an opportunity to find you. Create it by mastering the skills that dealerships crave. Build your success on a foundation of expert knowledge and professional confidence. Unlock your F&I potential and start your journey toward a six-figure income today.

ENROLL NOW and take control of your professional destiny!

You now have the f&i manager commission structure explained so you can stop guessing and start earning. Success in this office isn’t about luck; it’s about mastering the $1,500 PVR benchmark and managing chargebacks with surgical precision. You’ve seen how the draw works and why top performers command the highest percentage of the back-end gross. Now you need the technical roadmap to get there. Our training provides 180 days of digital access to a curriculum built from 20 years of real F&I office experience. You’ll master financing, insurance, and federal compliance through a proven system designed for immediate dealership results. Don’t leave your income to chance when you can invest in a skillset that pays dividends every single month. Your path to a six-figure career is clear. Are you ready to step into the most profitable role in the building? Master F&I and start your high-income career; ENROLL NOW!. You have the ambition. We have the blueprint. Let’s get to work.

Most F&I managers earn a commission between 10% and 17% of the total department gross profit. This f&i manager commission structure explained helps you see that your income scales directly with the value you create for the dealership. High performers in top tier retail environments can see their percentage climb to 20% or more when they hit specific volume bonuses. If you generate $120,000 in monthly gross, a 15% rate puts $18,000 in your pocket.

PVR stands for Per Vehicle Retail, and it’s the primary metric used to measure your efficiency in the F&I office. You calculate this figure by dividing your total monthly gross profit by the number of units sold. Successful managers aim for a PVR of $1,600 to $2,400 depending on the dealership’s brand and inventory. Tracking this number daily allows you to monitor your performance and maximize your monthly take home pay.

An entry-level F&I manager typically earns between $65,000 and $95,000 in their first 12 months. While you’re still building your skills, your income depends on your ability to close deals and protect dealership profit margins. Many graduates of professional training programs bypass this lower range and hit $115,000 within their first year by mastering advanced sales techniques early. Your potential is only limited by your drive to master the process.

A chargeback is a reversal of your earned commission that occurs when a customer cancels a product or pays off their loan within a specific timeframe. Most finance contracts include a 90 to 180 day window where the lender can claw back the reserve if the loan is refinanced or paid in full. You can minimize these losses by maintaining a chargeback rate below 8% through better product value presentation and thorough customer education during the signing process.

Most F&I roles are 100% commission or a performance-based structure with a small base salary of $2,500 to $3,500 per month. This f&i manager commission structure explained clarifies that your earning potential is uncapped, which is why it’s a sought-after position. You aren’t limited by a fixed hourly wage or a standard corporate salary cap. Your paycheck reflects your direct contribution to the dealership’s bottom line every single month.

A draw is a guaranteed minimum payment that acts as an advance against your future commissions to ensure you have steady cash flow. If your draw is $4,000 and you only earn $3,500 in commission during a slow month, the dealership pays you the full $4,000 but you’ll owe the $500 difference back from next month’s earnings. It’s a safety net that protects you during seasonal fluctuations while you focus on building your high income career.

You can increase your product penetration by using a structured 300% menu presentation on every single deal without exception. Top performers maintain a 2.0 product per deal average by identifying customer pain points within the first 7 minutes of the interview. Focus on the specific benefits of service contracts and GAP insurance to move your penetration rate from a 35% average to a 55% elite level. Mastering the menu is the fastest way to boost your PVR.

Investing in a professional F&I manager course is highly profitable because it shortens your learning curve by 12 to 18 months. Professionals who master compliance and sales psychology through structured training often see a $400 to $600 increase in their PVR immediately. This investment usually pays for itself within your first four deals. It provides the roadmap you need to unlock your full potential and secure a prestigious position in the automotive industry.