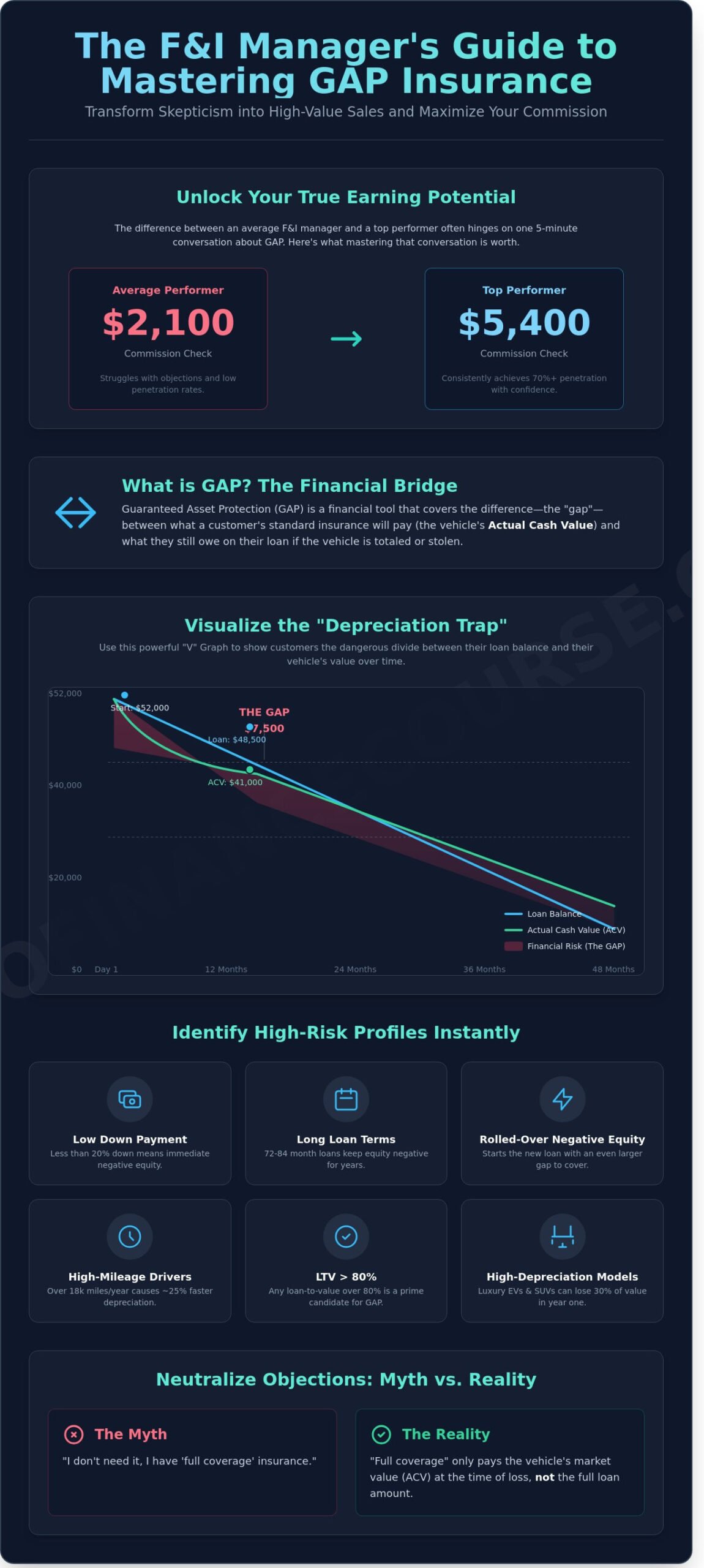

The difference between a $2,100 commission check and a $5,400 one often comes down to a single five minute conversation about a product your customer thinks is a scam. You know the thick tension that fills the office the moment you pivot to the menu. It is exhausting to fight through a wall of skepticism when you are trying to provide real value. You want to be the expert, but low penetration numbers and presentation anxiety are holding back your true earning potential.

We agree that the F&I office should be a place of professional pride, not a battleground of objections. This guide will teach you exactly how to explain gap insurance to customers using proven techniques that build immediate trust. You are about to unlock the specific skills needed to skyrocket your dealership profitability and secure the high income career you deserve. Your path to becoming a top performer starts with changing the narrative in your office.

We are breaking down the exact scripts and logic used by managers who consistently maintain a 70% or higher penetration rate. You will learn the roadmap to transform your approach, improve your CSI scores, and dominate the desk with total confidence.

You aren’t just selling a product. You’re securing a client’s financial future. In 2026, vehicle prices have plateaued at record highs, yet immediate depreciation remains a brutal reality. Learning how to explain gap insurance to customers starts with shifting your mindset from salesperson to financial protector. Guaranteed Asset Protection (GAP) serves as the vital bridge between a vehicle’s Actual Cash Value (ACV) and the remaining loan balance. Without it, a total loss becomes a financial catastrophe for your client. This GAP insurance overview highlights how this coverage has evolved to meet modern lending needs. Standard comprehensive insurance only pays what the car is worth, not what the customer owes. In a market where 18% depreciation occurs the moment the tires hit the curb, that difference is a massive liability.

Consider a 2026 mid-size SUV priced at $52,000. If a customer signs an 84-month loan with 5% down, they’re immediately caught in the “Depreciation Trap.” By month 12, the ACV might drop to $41,000, while the principal balance sits at $48,500. That $7,500 deficit is the “gap” they must pay out of pocket if the car is wrecked or stolen. Long-term financing, specifically terms ranging from 72 to 84 months, keeps equity negative for much longer than traditional 60-month cycles. GAP insurance is a specialized financial tool designed to provide absolute negative equity protection by settling the difference between an insurance payout and the total loan payoff.

Most buyers believe “full coverage” means they’ll get a brand-new car if theirs is destroyed. It doesn’t. Standard policies focus on current market value, not debt satisfaction. This confusion grows when customers roll over negative equity from a previous trade-in. A $4,500 carry-over balance makes GAP essential from day one. To succeed, you must master the art of transparency. Your goal is to align the dealership’s profitability with the customer’s long-term security. If you want to understand how this fits into your broader professional goals, review our F&I Manager Ultimate Career Explainer to see how elite managers drive value. Stop selling features and start selling solutions. Master how to explain gap insurance to customers to protect their credit and your reputation.

Stop guessing which customers need protection. Start analyzing the deal structure to identify high-risk profiles immediately. A top-performing F&I manager looks for specific triggers: low down payments, high-interest tiers, and extended loan terms. Buyers with credit scores below 640 often face higher rates, which means they pay down principal slower. This creates a massive window of vulnerability where the loan balance far exceeds the car’s actual value.

Knowing how to explain gap insurance to customers starts with identifying their specific risk profile before they even sit in your office. High-mileage drivers are prime candidates. If a customer drives over 18,000 miles per year, their vehicle’s value will drop roughly 25% faster than the national average. You must show them that their insurance payout won’t keep up with this accelerated depreciation. For “hot” vehicle models like luxury EVs or high-end SUVs, the depreciation cliff is even steeper; some models lose 30% of their value within the first 12 months of ownership.

Any loan with an LTV over 80% is a candidate for GAP. When you how to become an auto F&I manager, you learn that deal structuring is your best sales tool. If a customer rolls $3,000 of negative equity into a new $40,000 loan, they are starting at 107% LTV. Use their credit profile to justify the need. Position GAP as a “defense strategy” for their credit score. A total loss without GAP often leads to a defaulted loan, which can tank a credit score by 100 points or more overnight.

The 2026 market shows used car values stabilizing after years of record highs, meaning insurance payouts are getting smaller. Understanding how gap insurance works in a fluctuating economy is vital for your pitch. Leased vehicles almost always require this protection because the “gap” between the payoff and the residual value is a contractual liability for the driver. Many modern leases have it built-in, but you must verify this to provide expert guidance.

Master these qualifying details to drive your F&I profitability to new heights. Don’t wait for the customer to ask. Lead the conversation by showing them the “upside-down” risk inherent in their specific deal. It’s about protecting their investment and your dealership’s reputation. Are you ready to master these high-level skills?

Mastering how to explain gap insurance to customers is the fastest way to boost your PVR and secure your status as a top-tier F&I professional. You aren’t just selling a product; you’re providing a financial safety net. Learning how to explain gap insurance to customers using this framework ensures you don’t leave money on the table. Follow this 5-step roadmap to turn a complex concept into a common-sense decision for every buyer.

Drawing the gap is 10 times more effective than just talking about it. When you use the “Pencil” method to point at the $6,200 exposure on your graph, the customer sees the risk in black and white. Transparency is your greatest tool for success. Display your F&I menu clearly on a screen or printed sheet. This eliminates the “mystery” and positions you as a consultant rather than a salesperson. You’re showing them a roadmap to a high income career by building trust through visual clarity.

Stop talking about “paying off a dead horse.” That language feels like a total loss. Instead, explain how GAP helps them get into a new car immediately after an accident. Most professional GAP policies even cover up to $1,000 of their primary insurance deductible. This is a massive selling point that adds instant value. Use street-level English. Instead of saying “depreciation-driven deficiency,” say “the $5,800 hole the insurance company leaves in your pocket.” This simple shift makes the value proposition undeniable. If you want to master the skills needed for peak performance, focus on these clear, impactful conversations that drive profitability.

Mastering the F&I office requires more than just product knowledge. It requires the confidence to lead a customer through their own financial hesitation. To build a high-income career, you must learn how to explain gap insurance to customers by focusing on risk mitigation. You aren’t just selling a product; you’re providing a solution to a potentially devastating financial event.

Don’t let a customer’s loyalty to their insurance agent cost them thousands. Most standard policies only cover the Actual Cash Value (ACV) of the vehicle. If a $45,000 SUV is totaled and the market value is only $38,000, the customer is on the hook for that $7,000 difference. Use this script to clarify the risk:

Explain that even “New Car Replacement” riders often have strict limits. Many of these riders expire after 12 months or 15,000 miles. True GAP stays with the loan for the entire term.

Stop looking at the total price and start looking at the daily value. Most GAP policies cost less than 50 cents per day when rolled into a 72-month finance agreement. Frame the cost against the reality of a total loss. Ask the customer a direct question to shift their mindset.

“Could you write a $4,000 check today to clear a loan for a car you can’t drive?”

Most people realize they would rather pay the price of a small coffee each week than face a multi-thousand-dollar deficiency balance. This shift in perspective turns a “cost” into a strategic investment. You’re helping them protect their credit score and their future buying power. Expert F&I managers focus on this long-term profitability for the customer. It’s about providing massive value and building trust.

Ready to dominate the F&I office and maximize your earnings? Master the skills to start your high-income career today!

Your paycheck is a direct reflection of the value you provide at the desk. In the F&I office, GAP penetration is the primary engine driving your monthly commission. Managers who maintain a 55% GAP penetration rate consistently outearn those stuck at 25% by $2,500 or more every single month. When you master how to explain gap insurance to customers, you aren’t just selling a line item; you’re securing your own financial trajectory.

Professional confidence comes from deep product knowledge. If you’re hesitant, the customer feels it. Top-performing managers focus on “Education-Based Selling” because it removes the friction from the transaction. They don’t push; they inform. This shift in mindset transforms you from a “product pusher” into a trusted financial advisor. Mastering this specific skill set builds the foundation for a career that easily clears a $150,000 annual income.

High product penetration does more than pad your pockets; it strengthens your standing with lenders. Banks prefer “protected” paper. When your deals include GAP, lenders see a lower risk of default in the event of a total loss. This often results in better buy rates and faster funding for your dealership. Always prioritize ethics in your presentation to ensure long-term stability. F&I success is a marathon of consistency, not a sprint of high-pressure tactics. Stay compliant, stay transparent, and the profits will follow.

Self-study is the secret weapon of the top 1% of F&I managers. While others wait for the next “sales meeting,” elite managers spend 20 minutes a day refining their scripts and studying market trends. If you’re ready to stop guessing and start earning, you need a proven roadmap. Join the F&I Manager Training Course to unlock your full potential. You’ll learn exactly how to explain gap insurance to customers using high-conversion frameworks. Don’t leave your income to chance. Master the skills you need for a high-income career today and claim your spot at the top of the leaderboard.

Mastering how to explain gap insurance to customers isn’t just about closing a single deal; it’s about protecting a client’s financial health in a 2026 market where negative equity remains a primary concern. By using our four step framework and proven objection scripts, you can consistently boost your PVR by $500 or more per unit. Top managers who qualify their customers early see a 15% higher penetration rate on ancillary products compared to those who wait until the end of the menu presentation to start the conversation.

You’ve seen the roadmap, so now it’s time to build your professional engine. Our training is built from 20 years of real F&I office experience to ensure you master dealership-ready skills that work on the floor today. You’ll get 180 days of full access to our curriculum to join the ranks of 10,000 top-performing F&I managers nationwide who have transformed their income potential. Don’t leave your success to chance when you can follow a proven path to the top of the leaderboard.

Unlock Your High-Income Career: Enroll in the Online F&I Manager Course Now

Your journey toward becoming a prestigious, high-earning professional is ready for the green light.

The best way to explain GAP insurance to a first-time car buyer is by using the “Financial Bridge” analogy. Show them that if a $35,000 vehicle is totaled and the primary insurer only pays $28,000, they face a $7,000 debt. Master this explanation to protect your customer’s credit and build your reputation as an expert. It’s about turning a potential 5-figure loss into a zero-balance solution for their future.

Yes, GAP insurance remains negotiable in 2026, though most dealerships maintain a target profit margin of $450 to $650 per policy. State regulations in July 2025 have tightened, meaning price caps often range from $895 to $1,100 depending on your local jurisdiction. Successful managers focus on the value of the 150% LTV coverage rather than the price point. Use your skills to show the long-term savings.

Customers can buy GAP insurance after they leave the dealership, but they usually only have a 30-day window to secure it through their primary auto insurer. If they miss this 30-day mark, finding a standalone policy becomes significantly harder and often 25% more expensive. Learning how to explain gap insurance to customers before they drive off the lot ensures they get the best rate and immediate protection for their new investment.

GAP insurance treats a vehicle that is stolen and not recovered for 30 days as a total loss. Once the primary insurance company issues a settlement check for the current market value, the GAP policy kicks in to cover the remaining loan balance. This ensures the customer isn’t paying for a “ghost” car that no longer exists. It’s a vital protection for anyone living in high-theft metropolitan areas.

Most GAP policies automatically terminate when a customer refinances their loan because the original contract and account number no longer exist. If a customer refinances 14 months into a 72-month loan, they must purchase a new GAP policy to maintain coverage. Top managers use this as an opportunity to explain the importance of checking policy terms. It’s a critical step to ensure their financial success and master the F&I process.

Most modern GAP policies cover the primary insurance deductible up to a maximum of $1,000. This is a massive selling point when you’re mastering how to explain gap insurance to customers who are budget-conscious. If a customer has a $500 deductible, the GAP provider pays that amount directly as part of the total loss settlement. This saves the customer out-of-pocket expenses during a stressful time and reinforces the value of your expertise.

Dealerships typically earn a profit of $350 to $750 on each GAP policy sold at a retail price of $995. While the wholesale cost to the dealer might be as low as $295, the retail value reflects the convenience and high-limit coverage of a 150% LTV policy. Boosting your penetration rate to 55% or higher is a proven way to increase your department’s overall profitability and secure your high income career.

Dealership GAP is often superior because it covers up to 150% of the vehicle’s MSRP, whereas private insurance companies frequently cap coverage at 120%. For a customer with a 105% LTV loan plus taxes and fees, the dealer’s policy provides a more robust safety net. It’s a premium product designed for the specific risks of high-value automotive financing. Master these differences to position yourself as a sought-after professional in the F&I office.